Let’s be honest: debt feels like a heavy backpack you can’t take off. Whether it’s credit card balances that keep growing, a personal loan that’s hanging over your head, or that pesky store card from three years ago, debt has a way of draining your energy and your bank account.

If you’ve ever felt like you’re running on a treadmill: paying money every month but never getting anywhere: you aren’t alone. Most people try to pay a little extra here and there, but without a plan, that money just disappears into the void.

That is where the Debt Snowball Method comes in. It’s not just a strategy; it’s a psychological game-changer. It’s the method famous for helping millions of people finally see the light at the end of the tunnel.

In this guide, I’m going to break down exactly how the snowball method works, why it’s often better than other "math-heavy" strategies, and how you can start using it today to reclaim your financial freedom.

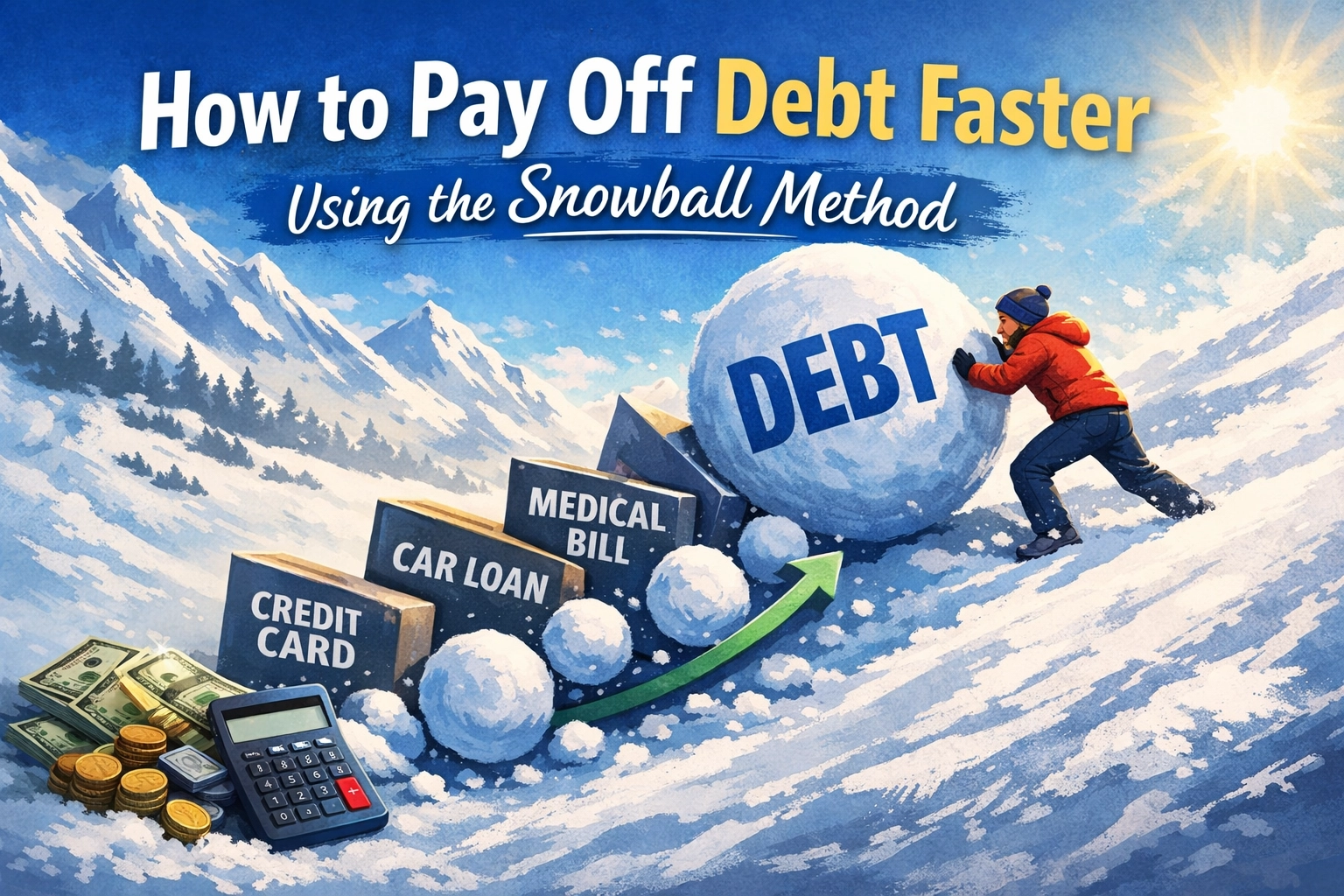

What is the Debt Snowball Method?

The Debt Snowball is a debt-reduction strategy where you pay off your debts in order from the smallest balance to the largest balance.

Wait, what about interest rates?

In the snowball method, you actually ignore the interest rates at first. I know that sounds crazy to some "math people," but there is a very specific reason for it. This method focuses on human behavior. When you see a small debt disappear quickly, you get a win. That win gives you the motivation to move on to the next one.

It’s called a "snowball" because of how it gains momentum. Think of a tiny snowball at the top of a hill. As it rolls down, it picks up more snow, gets heavier, and moves faster. By the time it hits the bottom, it’s an unstoppable force. Your debt repayment works the exact same way.

How to Set Up Your Debt Snowball in 5 Steps

Ready to get started? Grab a coffee, sit down with your statements, and follow these five steps.

Step 1: List Every Single Debt

Pull up your banking apps or look at your paper statements. List every debt you owe except for your mortgage. This includes:

- Credit cards

- Personal loans

- Medical bills

- Car loans

- Student loans

- Money owed to family or friends

Step 2: Organize from Smallest to Largest

Ignore the interest rates for a moment. Just look at the "Total Balance" column.

- Debt A: $450 (Store card)

- Debt B: $1,200 (Credit card)

- Debt C: $5,000 (Personal loan)

- Debt D: $12,000 (Car loan)

In this scenario, Debt A is your first target, regardless of whether it has a 10% or 25% interest rate.

Step 3: Pay the Minimum on Everything Else

You must keep your accounts in good standing. Set up automatic payments for the minimum amount due on every debt except the smallest one. This ensures you don't get hit with late fees and keeps your credit score protected while you focus your "attack" on one specific target.

Step 4: Attack the Smallest Debt

Determine how much extra money you can find in your budget. Maybe it’s $50 from skipping takeout, or $200 from a side hustle. Take that extra cash and throw it at the smallest debt on your list.

Keep doing this every single month until that debt is gone.

Step 5: The "Roll" Over

This is where the magic happens. Once Debt A is paid off, you don't just spend that extra money. You take the entire amount you were paying toward Debt A (the minimum + the extra) and add it to the minimum payment of Debt B.

Now you’re attacking Debt B with a much larger "snowball." Once Debt B is gone, you move all that money to Debt C.

The Secret Ingredient: Psychological Wins

You might be wondering: "Why wouldn't I pay off the debt with the highest interest rate first?"

That's called the "Debt Avalanche" method, and mathematically, it makes more sense. You save more money on interest that way. But here is the problem: Humans aren't robots.

If your highest-interest debt is a $25,000 student loan, and you start attacking it with an extra $100 a month, it’s going to take years before you see that balance disappear. Most people lose motivation and quit long before the debt is gone.

The Debt Snowball works because of dopamine. When you pay off a $400 credit card in two months, you feel like a champion. You’ve proven to yourself that you can win. That psychological "win" fuels your fire to keep going for the next twelve months.

In personal finance, behavior is 80% of the battle. The math is the easy part. The Snowball method tackles the behavior.

A Real-World Example

Let’s look at how this plays out for a typical household. Imagine you have three debts:

- Credit Card: $500 balance ($25 minimum payment)

- Medical Bill: $2,000 balance ($50 minimum payment)

- Car Loan: $10,000 balance ($250 minimum payment)

Total minimum payments: $325.

Let's say you find an extra $200 in your budget each month.

Month 1-2: You pay $225 ($25 min + $200 extra) toward the Credit Card. In just over two months, the credit card is GONE.

Month 3: Now you take that $225 and add it to the $50 you were already paying on the Medical Bill. You are now hitting that bill with $275 every month.

Month 10: The Medical Bill is paid off!

Month 11: Now you take that $275 and add it to the $250 you were paying on the car loan. You are now paying $525 a month toward your car.

See how it grows? By the time you get to the largest debt, you have a massive amount of cash available to crush it.

How to Find "Snowball Money"

The faster you can grow your snowball, the sooner you'll be debt-free. If you only pay the minimums, you’ll be in debt for decades. Here are a few ways to find extra cash to fuel your snowball:

- Audit Your Subscriptions: We all have them: streaming services, gym memberships we don't use, or app subscriptions. Canceling three $15 subscriptions gives you an extra $45 a month for your snowball.

- The "Sell One Thing" Rule: Go through your garage or closet. If you haven't used it in a year, list it on Facebook Marketplace. Even a $50 sale can jumpstart your first debt.

- Temporary Side Hustles: Driving for a ride-share app or doing freelance work for just six months can drastically shorten your debt-free timeline.

- Refinance High-Interest Loans: If you have high-interest debt, you might consider a debt consolidation loan with a lower interest rate: but only if you are disciplined. Use the lower interest to pay off the principal faster, not as an excuse to spend more.

Common Mistakes to Avoid

While the snowball method is simple, there are a few traps people fall into.

1. Not Having an Emergency Fund

Before you start your snowball, you should have a small "starter" emergency fund (usually $1,000 to $2,000). Why? Because life happens. If your car breaks down while you're paying off debt and you don't have cash, you'll just put the repair on a credit card and lose your momentum.

2. Stopping the Snowball Too Early

People often get through the first two small debts and then think, "I've got this under control, I can spend a little more now." Don't do it! The power of the snowball is the momentum. Keep that money rolling forward until the very last balance hits zero.

3. Ignoring Your Budget

You can't out-earn or out-snowball a spending problem. You need a monthly budget to ensure that the "extra" money you've earmarked for your debt actually goes there.

Is the Snowball Method Right for You?

The Debt Snowball is perfect for you if:

- You feel overwhelmed by the number of different payments you have to make.

- You need to see quick progress to stay motivated.

- You have several small-to-medium debts that are cluttering your financial life.

If you are someone who is incredibly disciplined and cares only about the math, the Debt Avalanche (paying highest interest first) might save you a few hundred dollars in the long run. But for the vast majority of us, the feeling of crossing a debt off the list is what actually gets us to the finish line.

Take the First Step Today

You don't have to be a financial genius to get out of debt. You just need a plan and the discipline to stick to it.

Tonight, sit down and make that list. Order them smallest to largest. Find your first target. Even if you only have an extra $20 this month, start the snowball. Once it starts rolling, you’ll be amazed at how fast it grows.

Freedom from debt isn't just about the money: it's about the peace of mind that comes with knowing you own your future, not the bank.