Let’s be honest: credit scores can feel a bit like that one subject in high school that everyone said was important, but nobody actually explained. You know it’s there, you know it’s important, and you know that if it’s "bad," you’re in trouble. But what actually goes into it? Is it a permanent record? And why does a three-digit number have so much power over your life?

If you’ve ever felt a bit lost looking at your credit dashboard, don’t worry. You aren’t alone. In this guide, we’re going to pull back the curtain and explain exactly how credit scores work in plain English. No jargon, no complicated math: just the facts you need to take control of your financial future.

The Secret Number That Runs Your Life

At its simplest, a credit score is a three-digit number, usually between 300 and 850, that tells lenders how likely you are to pay back borrowed money. Think of it as your financial "GPA." Just like a high school GPA tells a college if you’re a dedicated student, your credit score tells a bank if you’re a responsible borrower.

When you ask for a loan: whether it’s for a car, a house, or even just a credit card: the lender doesn’t want to read your entire life story. They want a shortcut. Your credit score is that shortcut.

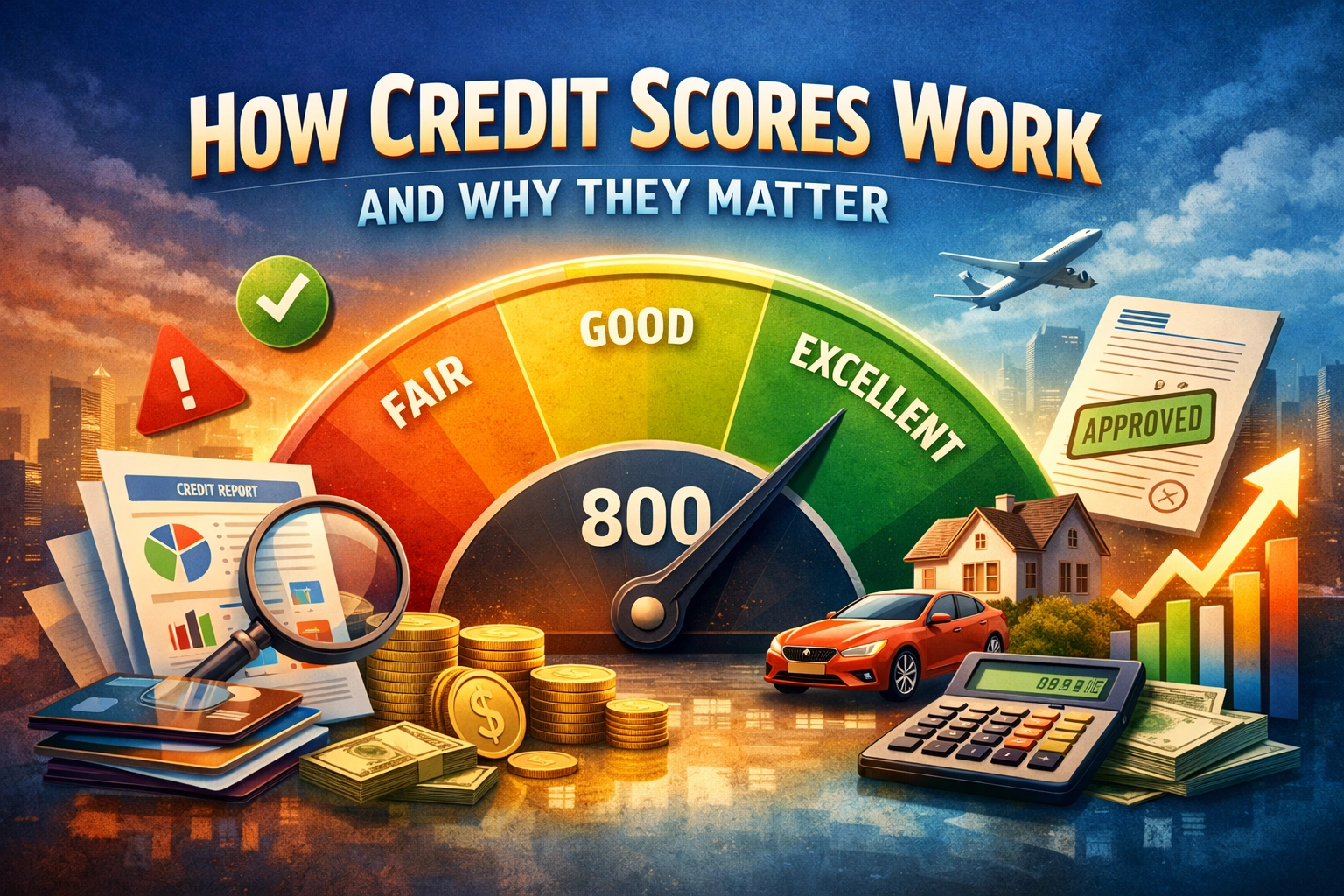

The Range: What’s Good and What’s Bad?

Most scores follow the FICO model, which looks like this:

- 300-579: Poor. You’ll likely struggle to get credit, or you’ll pay very high interest rates.

- 580-669: Fair. You can get approved, but you won't get the best deals.

- 670-739: Good. This is the "average" range. Most lenders are happy to work with you.

- 740-799: Very Good. You’re seen as a very low-risk borrower.

- 800-850: Exceptional. You’re the gold standard. You get the lowest interest rates and the best perks.

The Five Pillars: How Your Score Is Calculated

Your score doesn’t just pop out of thin air. It’s calculated based on data in your credit reports, which are maintained by three big companies: Equifax, Experian, and TransUnion. They look at five specific areas of your financial life.

1. Payment History (35%) – The Heavy Hitter

This is the single most important factor. Lenders want to know one thing above all else: Do you pay your bills on time? Even one late payment (usually 30 days or more past due) can cause your score to tank. If you have a history of paying on time, month after month, year after year, your score will reflect that consistency.

2. Amounts Owed / Credit Utilization (30%) – The Balance Act

This is where people often get confused. This isn't just about how much total debt you have; it’s about your credit utilization ratio.

Imagine you have a credit card with a $10,000 limit. If you consistently carry a balance of $9,000, you’re using 90% of your available credit. To a bank, this looks like you’re "maxed out" and might be struggling. However, if you only use $1,000 of that limit, your utilization is 10%. Keeping this number below 30% is the "magic rule" for a healthy score.

3. Length of Credit History (15%) – The Time Factor

In the world of credit, age matters. The longer you’ve had credit accounts open, the better. This is why financial experts often tell you not to close your oldest credit card, even if you don't use it much. Closing an old account shortens your average credit age, which can actually lower your score.

4. Credit Mix (10%) – The Variety Pack

Lenders like to see that you can handle different types of debt. Do you have a credit card (revolving credit) and a car loan (installment credit)? If you can manage both responsibly, it shows you’re a well-rounded borrower. You don't need to go out and get a loan just for the sake of variety, but it helps your score over time.

5. New Credit (10%) – The "Cool It" Factor

Every time you apply for a new loan or credit card, the lender does a "hard inquiry" on your report. This usually drops your score by a few points temporarily. If you apply for five credit cards in one week, it looks like you’re desperate for cash, and your score will take a bigger hit.

Why Does This Number Matter So Much?

You might be thinking, "I don't plan on buying a house anytime soon, so why should I care?" The truth is, your credit score affects way more than just bank loans.

Interest Rates: The Hidden Cost of a Low Score

The biggest reason to care about your score is the amount of money it saves you (or costs you) in interest.

Let’s say you’re buying a $30,000 car.

- Person A (Score of 750): Gets an interest rate of 4%. They pay about $3,100 in interest over five years.

- Person B (Score of 620): Gets an interest rate of 14%. They pay about $11,900 in interest over those same five years.

Person B pays $8,800 more for the exact same car just because of their credit score. That’s a lot of vacations or emergency savings lost to interest.

Renting an Apartment

Most landlords will run a credit check before they let you sign a lease. If your score is low, they might reject your application or ask for a much higher security deposit. In a competitive rental market, a good credit score is often the tie-breaker between you and another tenant.

Insurance Premiums

Believe it or not, in many states, car insurance companies use your credit-based insurance score to determine your rates. Statistically, people with higher credit scores tend to file fewer insurance claims. If your score is low, you might be paying more for your monthly car insurance premium without even realizing why.

Employment

Some employers, especially in the financial or government sectors, perform a credit check as part of the hiring process. They aren't looking at your exact score, but they are looking for signs of financial distress or irresponsibility. They want to know that the person they are hiring is reliable.

Common Credit Score Myths

Because credit scores are so important, there is a lot of misinformation out there. Let’s clear a few things up:

- "Checking my own score hurts it." False! Checking your own score is a "soft inquiry" and has zero impact. In fact, you should check it regularly to catch errors.

- "Carrying a balance on my credit card helps my score." False! You do not need to pay interest to build credit. Paying your balance in full every month is the best way to keep your score high and your wallet full.

- "Closing an old card will help my score." False! As we mentioned earlier, closing an account can actually hurt your score by reducing your available credit and shortening your credit history.

- "My income affects my score." False! Your credit report doesn't know if you make $20,000 or $200,000 a year. It only cares about how you manage the money you borrow.

How to Check Your Score (Without Panicking)

In 2026, checking your credit score is easier than ever. Most banks and credit card apps now provide your score for free every month. You can also use services like Credit Karma or Mint to track your progress.

Once a year, you are also entitled to a free copy of your full credit report from each of the three major bureaus via AnnualCreditReport.com. This is the "deep dive" version of your score, showing every account you’ve ever had. It’s a good idea to check this once a year to make sure there isn’t any fraudulent activity or simple errors (like a paid-off bill still showing as "unpaid").

The Bottom Line

Your credit score isn't a judgment of who you are as a person. It’s just a tool: a financial tool that can either open doors or keep them locked.

The good news? Your score isn't permanent. No matter where you are today, you can improve it. By paying your bills on time, keeping your credit card balances low, and being patient, you can build a score that works for you, not against you.

Managing your credit is one of the most powerful things you can do for your financial freedom. It’s the difference between struggling to get by and having the world of finance work in your favor. So, take a look at that number, understand what’s driving it, and start making those small, daily choices that lead to big, long-term results.