If you feel like your bank account has a leak, you aren’t alone. Even as we move through 2026 and see some of those wild inflation spikes finally start to settle down, the "new normal" of the cost of living is still pretty high. Most of us are looking at our screens, wondering where that extra $200 went last Tuesday.

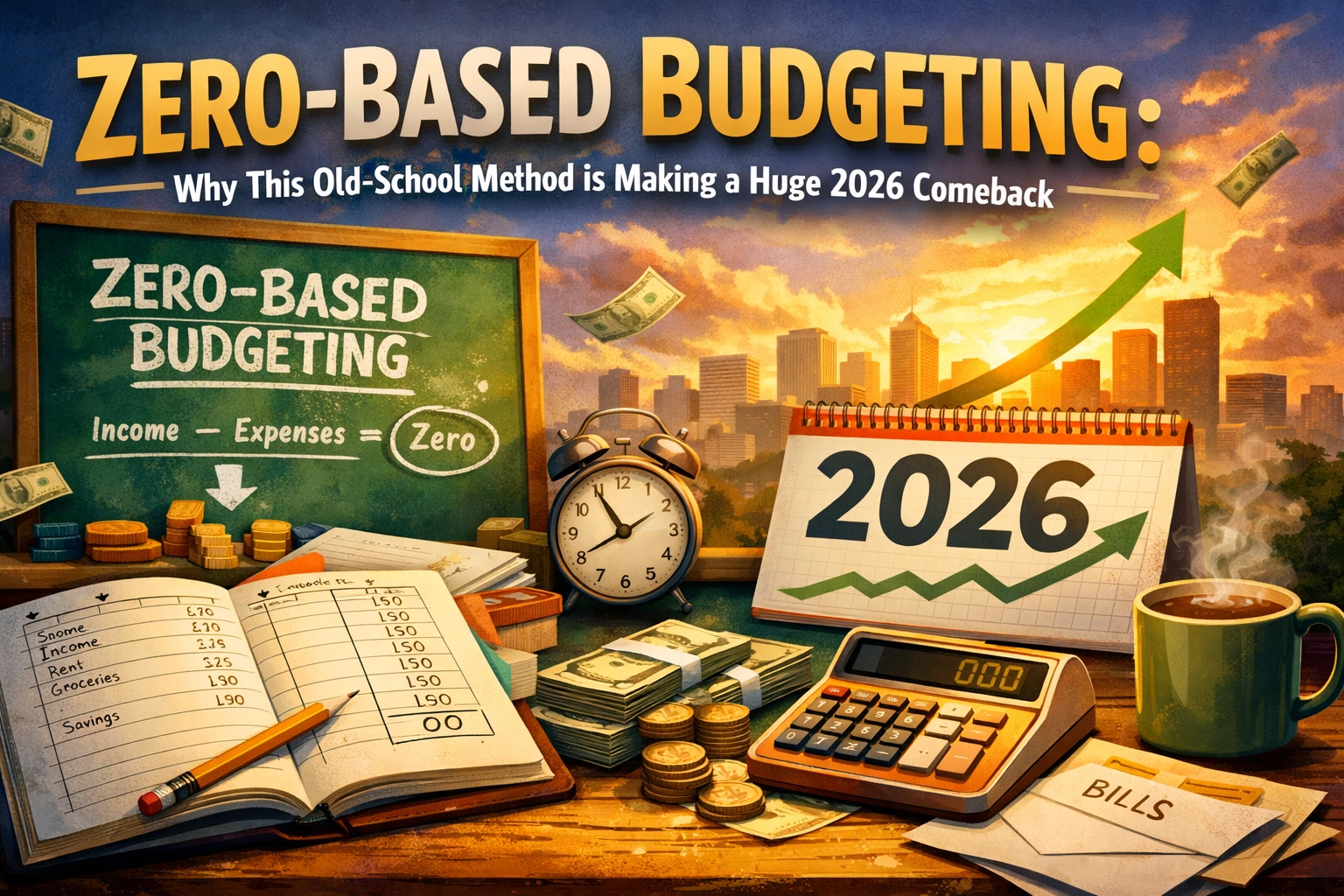

Enter the "old-school" hero of the personal finance world: Zero-Based Budgeting (ZBB).

While it might sound like something your grandpa did with a pencil and a ledger, ZBB is having a massive resurgence in 2026. Why? Because in an era of digital subscriptions, fluctuating interest rates, and AI-driven spending temptations, we need a method that forces us to look at every single cent.

In this post, we’re going to break down why Zero-Based Budgeting is the ultimate money move for 2026, how it works, and how you can use it to finally hit those big financial goals.

What Exactly is Zero-Based Budgeting?

Despite the name, Zero-Based Budgeting does not mean you have zero dollars in your bank account. That would be stressful! Instead, it means that at the end of the month, your Income minus your Expenses equals exactly Zero.

In a traditional budget, you might say, "I usually spend about $500 on groceries," and then just hope for the best. With ZBB, you give every single dollar a specific "job" to do before the month even begins. Whether that dollar is going toward rent, a high-yield savings account, a Netflix subscription, or your "fancy coffee" fund, it has to be assigned somewhere.

If you earn $4,000 this month, you need to tell all $4,000 exactly where to go. By the time you’re done planning, there should be nothing left unallocated.

Why ZBB is Winning in 2026

You might be wondering why people are flocking back to this method now. We have fancy banking apps and AI assistants that track our spending: so why go back to basics?

1. The "Subscription Creep" is Real

In 2026, everything is a subscription. From your car's heated seats to your grocery delivery and your five different streaming platforms, it’s easier than ever to lose $50 or $100 a month to services you don't even use. ZBB forces you to justify every expense from scratch every month. It’s the ultimate "delete" button for wasted money.

2. Economic Uncertainty and Strategic Shifts

As the research suggests, ZBB usually makes a comeback when things feel a bit unpredictable. While the 2026 economy is showing signs of stabilizing, the job market has shifted toward more freelance and "gig" work for many. When your income fluctuates, you can't rely on last month's budget. You have to build a new one based on what you actually have right now.

3. Combatting "Lifestyle Creep"

As inflation eases and some of us are seeing modest raises, there’s a massive temptation to just spend more. ZBB keeps you grounded. Instead of letting that extra $100 disappear into "miscellaneous" spending, ZBB forces you to decide: "Does this go to my 2026 debt payoff plan or my vacation fund?"

How to Build Your 2026 Zero-Based Budget

Ready to give it a shot? You don't need to be a math whiz. You just need a little bit of time and a clear head. Here is the step-by-step breakdown.

Step 1: Write Down Your Total Income

Include everything that hits your bank account. Your main salary, your side hustle payouts, that $20 your aunt sent you for your birthday: all of it. This is your "pot" of money for the month.

Step 2: List Your Fixed Expenses

These are the non-negotiables. Rent or mortgage, utilities, car payments, and insurance. In the 2026 landscape, pay close attention to your utilities: energy costs have been a bit of a rollercoaster lately, so use an average of your last three months.

Step 3: List Your Variable Expenses

This is where the magic happens. Groceries, gas, dining out, and entertainment. This is also where most people realize they are overspending. Be honest here. If you know you’re going to spend $100 on weekend drinks, put it in the budget.

Step 4: Don't Forget "The Jobs" for Your Savings

This is the most important part of ZBB. Savings, investments, and debt repayments are treated like "bills." You are paying your future self.

- Emergency Fund: Aiming for that 3–6 month cushion.

- Debt Payoff: Using the "Debt Snowball" or "Debt Avalanche" method.

- Investment Portfolios: Contributing to your 401k or Roth IRA.

Step 5: Do the Math (The Goal is Zero)

Subtract your expenses (Step 2, 3, and 4) from your income (Step 1).

- If you have money left over: You aren't done! Give that money a job. Put it toward debt or extra savings.

- If you are in the negative: You need to make some cuts. Maybe the "Dining Out" budget takes a hit this month so you can cover your electric bill.

The Benefits of Starting Now

The reason ZBB is such a powerful personal finance tool is that it creates accountability and transparency. When you have to defend every expense to yourself, you become a lot more intentional.

- Cost Efficiency: You’ll naturally start cutting out the "bloat."

- Strategic Allocation: Your money starts going toward what you actually care about, like a down payment on a house or a 2027 travel fund, rather than mindless scrolling-induced Amazon purchases.

- Better Forecasting: Because you’re looking at your budget every month, you’ll start to see patterns. You'll know exactly when those yearly insurance premiums are coming up and you won't be surprised.

ZBB vs. Traditional Budgeting

In traditional budgeting, you usually look at what you spent last month and adjust it by a little bit. "I spent $400 on food last month, let's try for $380 this month."

The problem? It assumes that last month was "correct."

ZBB assumes nothing. Every month is a fresh start. This is especially helpful in 2026 because our spending habits are changing so fast. Maybe you’re working from home more now, so your gas budget should be lower, but your home office/coffee budget is higher. ZBB lets you pivot instantly.

Tips for Success in the 2026 Digital World

While you can do this on a piece of paper, we live in 2026: let's use the tools at our disposal.

- Use an App: There are plenty of great Zero-Based Budgeting apps that sync with your bank accounts. They make the "tracking" part much easier.

- The "Buffer" Category: Life happens. Always include a small "Miscellaneous" or "Oops" category of about $50–$100. If you don't use it, put it toward savings at the end of the month.

- Check-in Weekly: Don't just set it and forget it. Spend 10 minutes every Sunday morning seeing where you stand. It prevents that "end of the month" panic.

Common Pitfalls (And How to Avoid Them)

The biggest complaint about ZBB is that it feels "too restrictive." If you feel like you can't breathe, you're doing it wrong.

The Fix: Make sure you are budgeting for fun! A budget isn't a straightjacket; it's a map. If you want to spend $200 on a new pair of shoes, put it in the budget. As long as the math equals zero at the end, you are allowed to spend your money on things that make you happy.

Another pitfall is forgetting those "once-a-year" expenses. Think about car registrations, holiday gifts, or annual software renewals. In a ZBB world, you should have a "Sinking Fund" for these. Save a little bit every month so when the big bill hits, the money is already there, waiting for its job.

Final Thoughts: Taking Control of Your Financial Future

As we navigate the 2026 economic landscape, the best thing you can give yourself is peace of mind. Financial stress usually comes from the unknown. When you don't know where your money is going, you feel out of control.

Zero-Based Budgeting puts the steering wheel back in your hands. It’s simple, it’s casual, and it’s incredibly effective. Whether you’re trying to crush debt, build wealth, or just stop worrying about your bank balance, giving every dollar a job is the way to go.

So, grab your favorite drink, open up your banking app, and start your first 2026 Zero-Based Budget today. Your future self will definitely thank you.